Get Flood Insurance Vermont & Save Money Too.

People in Vermont save on average $500 to $1,457+ on their annual flood premiums.

In many cases, we save them even more. Get the cheapest flood insurance in Vermont without sacrificing coverage.

featured on

Save Money Now On Your Flood Insurance Vermont

Floods can occur anywhere, at any time. It can be a distressing experience, particularly when contemplating the damage to your home and the ensuing costs of restoring normalcy. With the unpredictability of weather patterns bringing floods to unanticipated locations, it’s crucial to contemplate flood insurance for your home in Vermont. There are varying levels of protection available, contingent on your residence. Understanding the cost of flood insurance in Vermont is integral to safeguarding what is most valuable.

Our team of Flood Nerds possesses extensive knowledge in discerning all the available options for your property, enabling you to make an informed decision with confidence. A majority of our clients save between $500 – $2,500 on their Vermont flood insurance by opting for one of our numerous private flood insurance alternatives. Certain factors must be taken into account to ascertain the cost of flood insurance in Vermont.

For a precise estimate, we have devised a quick calculator below. However, for a dependable evaluation, we advocate obtaining a free quote, which only necessitates a few minutes to complete. Most of our clients in Vermont expend between $500 and $1,500 for home flood insurance. Discover the potential cost of flood insurance coverage for your Vermont home with us today.

Finding Cheap Flood Insurance in Vermont, the Flood Nerd™ Way

Securing affordable flood insurance in Vermont can seem overwhelming, but worry not; the flood nerds are at your service! If affordable flood insurance in Vermont is what you seek, then you’ve landed in the right spot. We scout for the most economical flood insurance policies that do not skimp on coverage and have access to several exclusive, affordable flood insurance companies in Vermont. Allow us to guide you through our process.

Step 1: Submit Your Information via Our Online Form Initiate your journey to affordable flood insurance in Vermont by providing your property information to your Flood Nerd through our online form. This enables us to evaluate your property and juxtapose it with the NFIP to guarantee you secure the most cheap flood insurance policy.

Step 2: Explore and Contrast Rates Avoid settling for the initial quote received from your local agent – permit a flood nerd to explore and contrast rates with our pre-approved options to confirm you’ve located a flood insurance company that, with the assistance of your flood nerds, offers a superior deal. The NFIP has monopolized flood insurance for decades, and now it’s the moment to economize in Vermont.

Step 3: Engage with Exclusive Companies As Flood Nerds specialize solely in flood insurance, we proffer more alternatives than most, and we maintain exclusive partnerships with several companies that present low-cost policies unattainable to an agent lacking flood insurance expertise in Vermont. This grants our clients access to additional savings opportunities unattainable elsewhere. By capitalizing on our exclusive partnerships, clients can conserve hundreds on their premiums while maintaining superior coverage and peace of mind, knowing their property is safeguarded against floods.

Obtaining premium flood insurance in Vermont need not be intricate or costly. With Flood Nerds by your side, you can rest assured that you’re acquiring excellent coverage without sacrificing coverage or service quality. We comprehend that every individual’s circumstance is unique, hence we endeavor to offer personalized solutions adapted to each client’s requirements and financial limitations. So, why delay? Reach out to us today, and let us assist you in discovering affordable flood insurance in Vermont!

Get Cheap Flood Insurance without Compromising Coverage

★★★★★

"Same Coverage at a Better Rate"

-Mohammed K

Flood Nerds will shop the private flood insurance markets and then compare them to the NFIP, guaranteeing you the better option. We will send you the cheapest flood insurance rates within minutes.

★★★★★

"Quick Response, Very Knowledgable"

– Robert W

Paying for low-cost flood insurance is awesome. And letting the Flood Nerds shop your property has other benefits – you can get better coverage while saving money, and you can get it fast.

★★★★★

"Would highly recommend Better Flood for your flood insurance needs."

– Varun K

Better Flood Insurance is an independent flood insurance broker that shops flood insurance ONLY. Flood Nerds are Flood insurance experts. We have 5000+ happy clients and 390+ 5-star reviews.

Vermont Flood Insruance

Does my Vermont homeowner insurance cover flooding?

A typical Vermont homeowners’ policy is written through Farmers, State Farm, Allstate, and Progressive, for instance, excludes flooding as something that will be covered under their homeowner’s policy.

In most cases, the only way to get flood coverage is by purchasing a stand-alone flood insurance policy. However, you should ask your homeowners agent if you can add an endorsement to your homeowner’s policy to cover flooding. Yet, don’t be too surprised if the answer is NO.

Do I need flood insurance in Vermont?

It is important to have flood insurance coverage in Vermont because our beloved Cowboy State has seen a fair share of flooding, and there is likely more coming.

We believe that most homeowners think about Flood insurance in Vermont at some point, maybe before buying a home, or during the closing process. However, many of us only think about it when a big storm is looming, or we have heard on the news that there is flooding forecasted or happening currently too close to our home.

If your home or business is in a flood zone, that is considered low flood-risk area. Sadly, many homeowners decide to forgo purchasing coverage because they believe they are safe from flooding. Some real estate agents and some insurance agents may even say you don’t need it.

I ask you to consider the facts: 20-percent of all flooding events across our nation come in areas that are considered low risk. After our last few major storms (Hurricane Harvey), we saw flooding in these low-risk areas. In 80 percent of these individuals, they had water in their home or buildings and didn’t have flood insurance coverage.

In Harris County, nearly 135,000 homes were damaged. Three-fourths of these properties were considered low to moderate risk.

Flooding in Vermont

We hear often that people believe that the government will help, and this is true. However, there are a few things that must align for you to get government assistance.

1 – The president of the United States must declare the flooding event a state of emergency. If this doesn’t happen, then there won’t be assistance.

2 – The average amount of assistance that homeowners get after a flood, when they do not have flood coverage, is $5,000. The average cost of damage to one’s property after a flood is $38,000+. That $5K you get from the government? It comes in the form of a loan and you will need to pay it back. Are you willing to gamble away your financial future by forgoing flood insurance coverage?

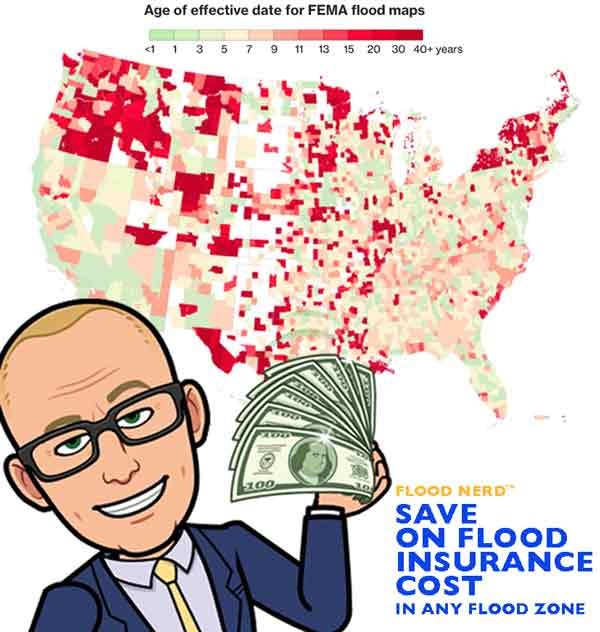

https://www.bloomberg.com/graphics/2017-fema-faulty-flood-maps/

One more note on these low-risk flood zone maps. Many of these maps are over 40-years old. If the area has been developed, then there is likely more concrete, creating a barrier for land that previously, might have absorbed the massive downpour.

Vermont Flood Zone Map

Because of all these factors, it is difficult for property owners to know their true risk of flooding. FEMA admits that their flood maps only give an idea for part of the risk. Our recent storms are facts that it can rain anywhere within Vermont, and you should consider getting flood coverage, so you are not uninsured when you need it most.

FEMA flood zone maps often take years to go into effect after the terrain was studied, this gives the impression that the area is “more up to date” then it really is.

The average cost for Vermont flood insurance in these Low-risk areas is $595 per year.

FEMA’s National Flood Insurance Program (NFIP) and all federally backed lenders rely on these Virginia flood insurance maps to assess risk, set premiums, and determine who is required to purchase flood insurance. Bad information about an area’s flood risk can leave property owners under or uninsured.

How much is flood insurance in Vermont?

Vermont NFIP flood insurance.

There are many options available in Vermont regarding flood insurance, but they basically fall into two main categories. The government option also called the NFIP or FEMA and the private flood insurance market

The National Flood Insurance Program (NFIP), also known as FEMA, which is the government option for flood insurance. The NFIP has enjoyed a 50-state monopoly on the flood insurance market.

Not “private flood insurance” but NFIP Resellers

Suppose you have Nationwide Flood Insurance, State Farm Flood Insurance, Progressive Flood Insurance, or any of the logos below. In that case, you are buying the NFIP flood policy that is just being resold through a government program. These companies are private companies, but their flood insurance is not. Here is a list of the 70 companies that resell the NFIP policy.

Vermont private flood insurance market

There are alternatives to the NFIP or government insurance. It is called Private flood insurance, most notably Lloyds of London Flood insurance. However, there are other options available in Virginia. We shop all the options for your property in your region to ensure you are getting the best premium. If you are ready to have us do the work for you, please click here.

Our shopping does include the NFIP because sometimes we find that with government subsidies, you can get a much better premium.

Virginia flood insurance quote

Lloyds of London Flood Insurance Vermont Market

Vermont is fortunate to have many Lloyds of London flood insurance options. Although many Lloyds flood insurance companies will have you assume that there is only one option, nothing could be further from the truth.

Lloyds of London has a rich history and is attributed to have invented the very first modern insurance model. Unlike most of its competition, Lloyds of London is not really a company but rather a corporate body. This structure works quite well since it has been around for over 330 years. Lloyds operates under multiple financial backers that all pool their capital to spread the risk.

I have two blog posts that take a deep dive into Lloyds of London and what they mean to Vermont ’s flood insurance market. If you are interested, the links are below.

Lloyds of London Flood Insurance

FEMA vs Private flood insurance

Lloyds also insures the world for flood insurance, meaning they cover flooding events in India, Australia, and much of Europe. The “game” of insurance is to spread your risk since Lloyds is worldwide.

My joke here is that Lloyds is banking on God’s promise that he won’t flood the entire world again, …..so they won’t have to pay out the whole world’s flood claim.

There are many factors that go into getting the cost of flood insurance for Vermont. If your home is in what is considered low-to-moderate risk, you can get a heavily subsidized policy though the government.

Vermont flood insurance low-to Moderate Risk rate and cost.

This is Flood Zone X, which is not lender required flood zone.

This is usually identified as an X-flood zone. Then we would suggest the government Preferred Risk Policy (PRP) which is a subsidized policy and has set flood insurance coverage limits (see grid below):