Everyone Saves Money on Flood Insurance with a Flood Nerd.

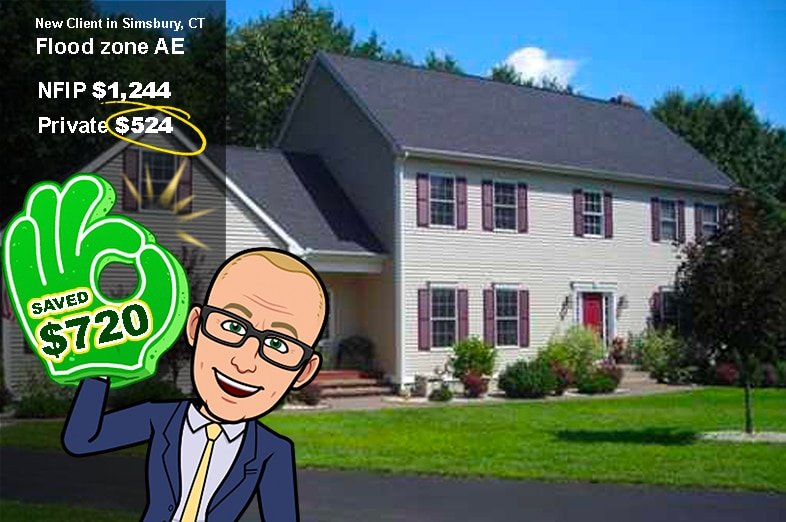

Your private flood premiums should be between $492 – $1,392 a year.

If You Are Paying More – Get A Flood Nerd™ Shopping Now.

featured on

Optimize Your Flood Zone Insurance Costs in 2023 with Expert Guidance

Uncover savings on your flood insurance by consulting with a dedicated Flood Nerd.

My name is Robert Murphy, and I’m here to secure you significant savings on your flood insurance. While I may appear to be your everyday insurance agent, I lead an elite team known as Flood Nerds. Our expertise isn’t hidden despite our considerable knowledge—because you’ve discovered us right here, accessible to all. Are you ready to navigate the complexities of flood zone coverage with us?

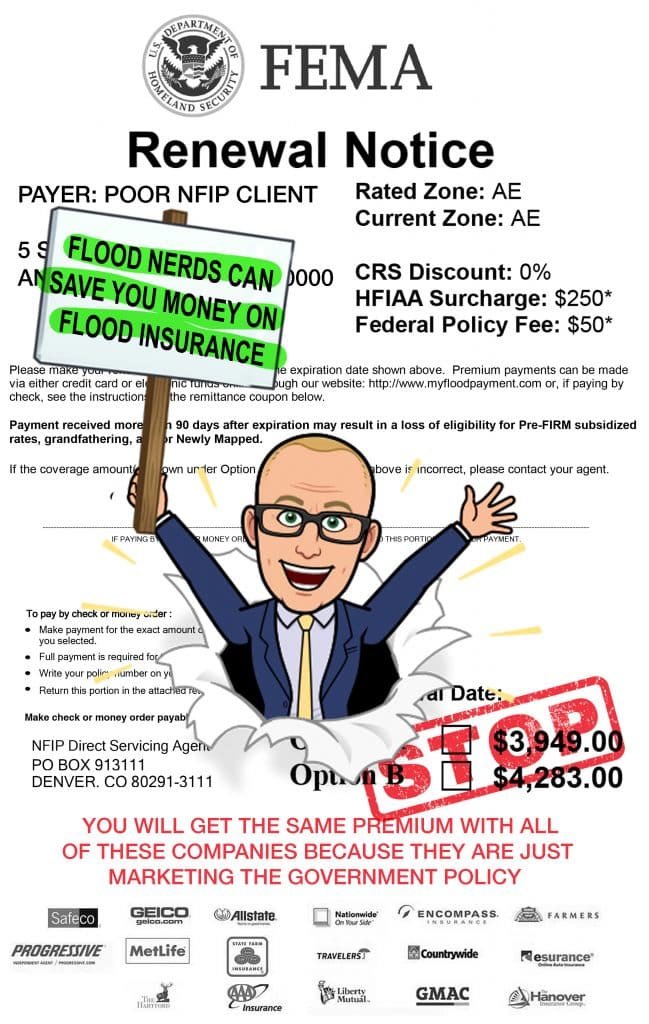

Shattering Myths: Beyond the NFIP's Reach for Flood Zone Coverage

Many assume that the only flood insurance solution lies with the NFIP, a misconception that used to color my perspective as well. However, a pivotal encounter nine years back revealed a profound truth: the untapped potential of the private flood insurance market is often overlooked by general insurance agents. Instead of exploring this avenue, they routinely default to the NFIP, bypassing opportunities to significantly reduce costs for their clients.

Such agents, whom I refer to as Flood Wimps, unintentionally endorse a monopolistic approach to flood zone insurance, doing a disservice to those seeking fair coverage and rates. It’s not a question of intent; it’s a gap in expertise.

Expanding on this, it’s crucial to understand that private flood insurance can be tailored to meet diverse needs and offer more competitive rates. By not presenting clients with these personalized options, agents inadvertently perpetuate the cycle of over-reliance on the NFIP. It’s a cycle I am committed to breaking, offering a more informed choice to those living in flood zones. The right knowledge can empower property owners to make better insurance decisions, ensuring they’re not just covered, but are financially protected with the best possible plan for their specific situation.

This realization ignited a fire within me, leading to my transformation into the Flood Nerd you see today. I recognized a chance to liberate individuals from the constraints of governmental flood programs, guiding them towards the competitive realms of private flood insurance.

Armed with the necessary education, resilience, and a relentless spirit, I embarked on a mission to dismantle the stronghold of government-sanctioned flood insurance. My battle prowess lies in securing unbeatable rates and superior coverage for your property.

I’m not a lone warrior in this fight. I’ve assembled a formidable squad of like-minded Flood Nerds, united by a fervent desire to rectify the injustices of exorbitant flood insurance premiums and inadequate policies. Whether you’re an existing policyholder, a prospective homeowner, a real estate professional, a lender, or a property manager, our team is your ally. We’re here to deliver savings, and we’re ready to prove it to you.

Securing Savings on Current Flood Zone Policies

Are you facing the burden of escalating NFIP flood insurance renewal premiums? You’re not alone in this challenging situation. Many find themselves caught in the upward spiral of costs associated with government-issued flood policies.

Take the first step towards financial relief by reaching out to us. By completing our contact form, you’ll engage a Flood Nerd who’s dedicated to advocating for your financial interests. We’re not just insurance agents; we’re specialists in the field of flood insurance, equipped with the expertise to find you the savings you deserve.

Our process involves a thorough examination of your current policy, identifying potential avenues for cost reduction. We don’t stop there; we proactively compare your coverage with offerings on the private market, where competition drives more favorable terms.

With over 40+ private flood insurance providers in our arsenal, our knowledge is extensive and our network, vast. We leverage this to negotiate the most advantageous terms for you. It’s not just about finding a lower premium; it’s about ensuring that your coverage meets your needs without compromising on protection.

Lastly, we understand the unique challenges and concerns that come with residing in a flood zone. Our mission extends beyond savings; we aim to provide peace of mind. With a Flood Nerd by your side, you can rest assured that your flood insurance is cost-effective, strong, and tailored to the intricacies of your property and location. Don’t let flood insurance premiums inundate you—let us build you a financial levee.

Embarking on this journey with a Flood Nerd means you’re choosing an advocate who will fight for not just affordability, but also for the assurance that comes with robust flood zone coverage. Our commitment is to empower you with options that reflect the true value of your property and the risks it faces. With our guidance, you can navigate the flood insurance landscape with confidence, secure in the knowledge that your home or business is protected by a cost-efficient and effective policy. We don’t just find you savings; we bring you security and clarity in the often murky waters of flood insurance.

Navigating Flood Zone Insurance for New Homeowners with Flood Nerds

The journey to owning your dream home shouldn’t stumble at the hurdle of high flood insurance costs. If you’ve just learned that your prospective haven lies in a flood zone, don’t let the potential for sky-high premiums cloud your excitement.

Avoid the default route to an overpriced NFIP policy. With Flood Nerds, you’ll get the necessary coverage without the hefty price tag, keeping your home purchase and closing process smoothly on course.

Tackling flood zone insurance solo can lead to unnecessary expenses. In contrast, allowing a Flood Nerd to guide you ensures savings and a stress-free path to closing on your home. We specialize in helping homebuyers like you celebrate the joy of a new home, free from the burden of inflated insurance premiums. With us, securing a flood zone policy is an investment in peace of mind, ensuring your home is safeguarded without derailing your finances.

Streamlining Closings for Real Estate Agents with Flood Nerd Expertise

As a real estate agent, maintaining momentum towards a smooth closing is crucial. Flood Nerds are here to ensure flood insurance doesn’t slow you down. Partner with us, and consider flood insurance handled.

Provide us with the property specifics, and we’ll swiftly secure the necessary documents, pinpoint the best prices, and lock in optimal coverage. This leaves you free to focus on your next client, knowing we have this one in safe hands.

Our proficiency in flood insurance extends to all property types, including coastal areas and vacation homes. Even when excess limits coverage is a factor, we navigate the terrain to uncover savings.

When flood insurance costs and requirements threaten to overwhelm your clients, introduce them to the Flood Nerds. We’re not just problem solvers; we’re your strategic partner in keeping every deal headed steadfastly towards closing.

Looking to differentiate your services in competitive markets? We have innovative strategies to share.

Get in touch at 866-990-7482 or send an email to connect and explore how we can enhance your real estate offerings.

Streamlining Flood Zone Compliance for Lenders and Loan Officers

Navigating the complexities of loan documentation and underwriter satisfaction can be daunting, particularly when dealing with properties in high-risk flood zones. This is where Flood Nerds come into play, offering expert assistance to ease the burden.

Our enthusiasm for flood insurance translates into providing you with all the necessary details, ensuring your closings stay on track and flood insurance costs remain manageable. This diligence helps maintain borrower eligibility and loan viability.

As Flood Nerds, we possess in-depth knowledge of the regulations surrounding lending for properties in flood zones. No matter the level of flood risk, we’re dedicated to finding coverage and premium options that satisfy all parties involved: buyers, sellers, and lenders alike.

Leveraging our access to a wide array of over 40+ top-tier insurers in the independent flood insurance market, we’re adept at securing the most competitive rates. Trust us to bring you compliance without complication, ensuring a seamless process for every property in a flood zone.

For mortgage lenders seeking seamless flood zone solutions, reach out at 866-990-7482 or via email to discover how we can augment your lending services. Our expertise in flood insurance ensures your clients’ needs are met efficiently and effectively.

Navigate Flood Zone Insurance with Ease

The realm of flood insurance can seem labyrinthine, with its ever-evolving government regulations, perplexing maps, and the NFIP’s fluctuating premiums. For homeowners in flood zones, this complexity can be more than just a nuisance—it can be a source of real concern.

That’s where our Flood Nerds come in, ready to demystify the process for you. By engaging our services, you’re not just hiring an insurance agent; you’re enlisting a dedicated specialist who will evaluate your specific situation, decipher the jargon, and translate it into a policy that fits your unique needs.

We understand that living in a flood zone comes with its own set of challenges, and flood insurance is a significant one. Our goal is to alleviate the stress associated with these policies. We don’t just find you coverage; we find you peace of mind.

With personalized attention and tailored solutions, we ensure that your flood insurance is more than a mandate—it’s a shield that protects your home and financial well-being. Our expertise is not only in finding the best rates but also in understanding the intricacies of flood zone requirements.

So, let a Flood Nerd take the helm of your flood insurance concerns. We’re here to ensure that your home is safeguarded, your costs are contained, and your mind is at ease, no matter what changes come your way. Contact us, and together, we’ll navigate the flood insurance waters, keeping you buoyant and secure.