Get Flood Insurance South Dakota & Save Money Too.

People in South Dakota save on average $500 to $1,457+ on their annual flood premiums.

Get flood insurance from a Flood Nerd® at Better Flood Insurance® and save big time.

featured on

Save money on flood insurance in South Dakota today.

Get Cheap Flood Insurance without Compromising Coverage

★★★★★

"Same Coverage at a Better Rate"

-Mohammed K

Flood Nerds will shop the private flood insurance markets and then compare them to the NFIP, guaranteeing you the better option. We will send you the cheapest flood insurance rates within minutes.

★★★★★

"Quick Response, Very Knowledgable"

– Robert W

Paying for low-cost flood insurance is awesome. And letting the Flood Nerds shop your property has other benefits – you can get better coverage while saving money, and you can get it fast.

★★★★★

"Would highly recommend Better Flood for your flood insurance needs."

– Varun K

Better Flood Insurance is an independent flood insurance broker that shops flood insurance ONLY. Flood Nerds are Flood insurance experts. We have 5000+ happy clients and 390+ 5-star reviews.

Does my South Dakota homeowner insurance cover flooding?

A typical South Dakota homeowners’ policy is written through Farmers, State Farm, Allstate, and Progressive, for instance, excludes flooding as something that will be covered under their homeowner’s policy.

In most cases, the only way to get flood coverage is by purchasing a stand-alone flood insurance policy. However, you should ask your homeowners agent if you can add an endorsement to your homeowner’s policy to cover flooding. Yet, don’t be too surprised if the answer is NO.

Do I need flood insurance in South Dakota?

It is important to have flood insurance coverage in South Dakota because our beloved Cowboy State has seen a fair share of flooding, and there is likely more coming.

We believe that most homeowners think about Flood insurance in South Dakota at some point, maybe before buying a home, or during the closing process. However, many of us only think about it when a big storm is looming, or we have heard on the news that there is flooding forecasted or happening currently too close to our home.

If your home or business is in a flood zone, that is considered a low flood risk area. Sadly, many homeowners decide to forgo purchasing coverage because they believe they are safe from flooding. Some real estate agents and some insurance agents may even say you don’t need it.

I ask you to consider the facts: 20-percent of all flooding events across our nation come in areas that are considered low risk. After our last few major storms (Hurricane Harvey), we saw flooding in these low-risk areas. In 80 percent of these individuals, they had water in their homes or buildings and didn’t have flood insurance coverage.

In Harris County, nearly 135,000 homes were damaged. Three-fourths of these properties were considered low to moderate risk.

We hear often that people believe that the government will help, and this is true.

However, there are a few things that must align for you to get government assistance.

1 – The president of the United States must declare the flooding event in a state of emergency. If this doesn’t happen, then there won’t be assistance.

2 – The average amount of assistance that homeowners get after a flood when they do not have flood coverage, is $5,000. The average cost of damage to one’s property after a flood is $38,000+. That $5K you get from the government? It comes in the form of a loan and you will need to pay it back. Are you willing to gamble away your financial future by forgoing flood insurance coverage?

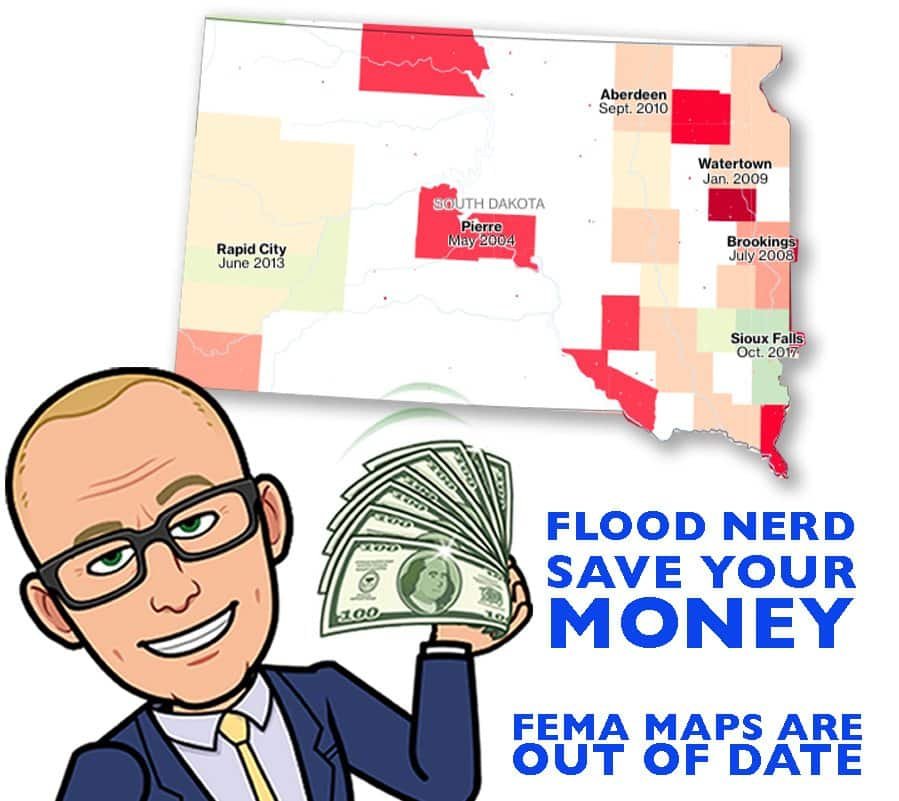

One more note on these low-risk flood zone maps. Many of these maps are over 40 years old. If the area has been developed, then there is likely more concrete, creating a barrier for land that, previously, might have absorbed the massive downpour.

Because of all these factors, it is difficult for property owners to know their true risk of flooding. FEMA admits that their flood maps only give an idea of part of the risk. Our recent storms are facts that it can rain anywhere within Tennessee, and you should consider getting flood coverage so you are not uninsured when you need it most.

FEMA flood zone maps often take years to go into effect after the terrain was studied; this gives the impression that the area is “more up to date” than it is.

The average cost for South Dakota flood insurance in these Low-risk areas is $595 per year.

FEMA’s National Flood Insurance Program (NFIP) and all federally backed lenders rely on these South Dakota flood insurance maps to assess risk, set premiums and determine who is required to purchase flood insurance. Bad information about an area’s flood risk can leave property owners under or uninsured.

How much is flood insurance in South Dakota?

South Dakota NFIP flood insurance.

There are many options available in South Dakota regarding flood insurance, but they basically fall into two main categories. The National Flood Insurance Program (NFIP also referred to as FEMA) we call I the government option, and the private flood insurance market.

The National Flood Insurance Program (NFIP), also known as FEMA, which is the government option for flood insurance. The NFIP has enjoyed a 50-state monopoly on the flood insurance market.

Not “private flood insurance” but NFIP Resellers

If you have Nationwide Flood Insurance, State Farm Flood Insurance, Progressive Flood Insurance, or any of the logos below then you are buying the NFIP flood policy that is just being resold through a government program. These companies are private companies, but their flood insurance is not. Here is a list of the 70 companies that resell the NFIP policy.

South Dakota private flood insurance market

There are alternatives to the NFIP or government insurance. It is called Private flood insurance most notably Lloyds of London Flood insurance, however, there are other options available in South Dakota. We shop all the options for your property in your region to ensure you are getting the best premium. If you are ready to have us do the work for you, please click here.

Our shopping does include the NFIP because sometimes we find that with government subsidies you can get a much better premium.

Lloyds of London Flood Insurance South Dakota Market

South Dakota is fortunate to have many Lloyds of London flood insurance options. Although many Lloyds flood insurance companies will have you assume that there is only one option, nothing could be further from the truth.

Lloyds of London has a rich history and is attributed to have invented the very first modern insurance model. Unlike most of its competition, Lloyds of London is not really a company but rather a corporate body. This structure works quite well since it has been around for over 330 years. Lloyds operates under multiple financial backers that all pool their capital to spread the risk.

I have two blog posts that take a deep dive into Lloyds of London and what they mean to South Dakota’s flood insurance market. Iif you are interested, the links are below.

Lloyds of London Flood Insurance

Private flood insurance vs NFIP

Lloyds also insures the world for flood insurance, meaning they cover flooding events in India, Australia as well as much of Europe. You see the “game” of insurance is to spread your risk since Lloyds is worldwide.

My joke here is that Lloyds is banking on God’s promise that he won’t flood the entire world again, …..so they won’t have to pay out the whole world’s flood claim.

How much does flood insurance cost in South Dakota?

There are many factors that go into getting the cost of flood insurance for South Dakota. If your home is in what is considered a low-to-moderate risk, you can get a heavily subsidized policy though the government.

South Dakota flood insurance low-to Moderate Risk rate and cost.

This is Flood Zone X, which is not the lender required flood zone.

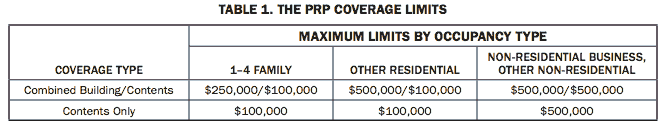

This is usually identified as an X-flood zone. Then we would suggest the government Preferred Risk Policy (PRP) which is a subsidized policy and has

The average cost for flood insurance in South Dakota with the maximum set limits in these Low-risk flood zone areas is $405 – $700 per year.

If your property is in a higher-risk flood zone, it is usually identified with a Flood Zone AE. Your lender will require you to have flood insurance. The cost of flood insurance in South Dakota depends on many factors that are unique to the structure. We are going to try to give you an idea for the most common homes we see in South Dakota with a basement.

We will look at the South Dakota cost of flood insurance for the NFIP maximum of $250,000 for the (building only) with NO CONTENTS and our recommended deductible of $5,000.

We will be rating this example on the NFIP, as well as on a few of our private flood insurance policies, specifically Lloyds flood insurance options in South Dakota.

Cost of Flood Insurance in SOUTH DAKOTA in high-risk flood zone AE

Our example is in Sioux Falls, but the premiums will be the same if in Union, Watertown, Aberdeen, or Rapid City, and many other South Dakota flood zones.

In our example, the Base Flood Elevation (BFE is 1401) and is a home that is built before 1973

NFIP option in South Dakota Flood Zone AE

NFIP – Coverage of $250,000 building coverage (no Contents coverage) and $5,000 deductible

NFIP Annual premium in High-Risk flood zone is $ 2,634.00

This option is what we see if the property has had a flood loss before and either doesn’t have an Elevation Certificate applied or the Elevation certificate shows that the lowest floor is 4 feet under the BFE for the area. You can use 10% of your coverage to cover other structures on your property.

South Dakota Private flood insurance – Lloyds of London Flood Insurance (option 1)

Coverage of $250,000 building coverage (no Contents coverage) and $5,000 deductible

Lloyds of London (option 1) Annual premium in High-Risk flood zone is $949.7

This option is great, and we are very happy when we can get this option. They can be a bit choosey about what risk they will accept and will not take anything that has had a flood loss. They offer basements coverage, about $2,000 for loss of use, and $2,000 for other structures, but they can’t increase this coverage. They do not require an Elevation Certificate to rate.

South Dakota Private flood insurance – Lloyds of London Flood Insurance (option 2)

Coverage of $250,000 building coverage (no Contents coverage) and $5,000 deductible

Lloyds of London (option 2) Annual premium in High-Risk flood zone is $ 1,033.57

This option is great, and we are very happy when we can get this option for our clients as well. They seem to be writing almost all risks; however, they do not write any property that is in a designated floodway or has the depth of -4 under the BFE. In our example, with our BFE being 5368, if the lowest floor is 5364, then they will not accept this risk. They will not take anything that has had a flood loss. They do offer limited coverage for basements and do not require an Elevation Certificate to rate, and as a percentage of coverage for loss of use. If you want coverage for other structures, then that will need to be added.

Private Flood insurance option (option 3) Not Lloyds

Coverage of $250,000 building coverage (no Contents coverage) and $5,000 deductible

The annual premium in High-Risk flood zone is $2,371.00

This option will take properties that have had one flood loss as long as it has been more than five years and the payout was under $100,000 on the claim. Their coverage matches the NFIP. They will write practically all risks, don’t need an elevation certificate to rate, and are a bit lower in premium than the NFIP.

Private Flood insurance – Lloyds of London (option 4)

This option must be written on the building’s Replacement Cost Value (RCV). Otherwise, there is a co-insurance penalty that kicks in. So, $250,000 might be a bit low in California, but to keep this going, let’s just use that for this option

Coverage of $250,000 (RCV) building coverage, No Contents, and a $5,000 deductible

The annual premium in the High-Risk flood zone is $ 693.24(great price).

This options rating system is all over the board. Sometimes we get a crazy great price, but other times the premium is way higher than the NFIP will consider taking a property that has had one flood loss before as long as it has been more than ten years and the payout was under $50,000 on the claim. Their preferred coverage is at replacement cost, which is slightly different from some of our other Lloyd’s flood options. We usually reserve this one if the property doesn’t fit the above options. We can adjust coverages to control premiums. As mentioned before, these underwriters’ rates are all over the board. It is worth shopping to ensure we get you the best premium possible. They don’t need an elevation certificate to rate.

Private Flood insurance – Lloyds of London (option 5)

Coverage of $250,000 (RCV) building coverage, No Contents, and $5,000 deductible.

The annual premium in High-Risk flood zone is $ 1,271.71

This option came from the company running the NFIP program, so the coverage matches the NFIP coverage with two differences. They offer living expenses which will cover your cost when you are displaced from your home during repairs (most Lloyds flood policies offer this). They also offer swimming pool clean out, which is kind of unique so if you have a pool, ask for this coverage.

Private Flood insurance – Lloyds of London (option 6)

Coverage of $250,000 (RCV) building coverage. No Contents and $5,000 deductible.

The annual premium in High-Risk flood zone is $ 753.00

This options rating system is also all over the board. Sometimes we get a crazy low price; other times the premium is way higher than the NFIP. They will consider taking a property that has had one flood loss before as long as it has been more than ten years and the payout was under $25,000 on the claim. They have been rumored to give a low price the first year and then non renew the following years or sometimes they jack the price way up so we will watch them. They have a slick system, and their underwriting is managed by a 3rd party, which also seems to be a glitch sometimes.

There are more options coming online every day, and we are working to be looking into every viable option.

Currently, South Dakota has 3,346 NFIP policies in force to date with the total cost of $3,115,261. That would make the average for South Dakota $931. Of course, some will pay more, and some will pay less.

Click here to have us shop and save you money.

Hello, South Dakota! Thanks for visiting our page for all your flood insurance needs. Let’s start with Brookings and Bruce, South Dakota. Brookings and Bruce have a combined total of 109 active flood policies. These policies add up to $120,428 in premiums. The average flood rate for Brookings and Bruce, South Dakota is $1,105.

Aberdeen’s average rate drops a little computing out to be $974. This includes 163 active flood policies with $158,832 in written premiums in Aberdeen, South Dakota.

Looking at Brown, Belle Fourche, Butte, Clark, and Codington South Dakota, we see these areas have 104 active flood policies with $75,738 in written premiums. The average flood rate for these areas is $728.

There are 428 active flood policies in Watertown, South Dakota, which is the highest in the state! The average flood rate here is $876. This includes $375,104 in written premium. Thanks for checking us out Watertown!

In Custer, Hermosa, Davison, Mitchell, and Day, South Dakota, the average flood rate is $728. The total number of flood policies in effect in these areas is 120 with $87,331 in premiums.

Moving on to Fall River, Philip, Castlewood, and Hamlin, South Dakota, we see an average flood rate for these areas is $767. The premiums written here total $62,926 with 82 active flood policies.

59 flood policies make up Blunt and Pierre, South Dakota. The average flood rate here is $972. The total written premiums for these areas are $57,330.

When we check out Lake and Madison, South Dakota, we find 155 active flood policies and a total of $134,886 in premiums. This allows the average flood rate to be $870 in Lake and Madison!

Deadwood, Lawrence, and Spearfish, South Dakota – your average rate is a little higher in your area – coming in at $1,203. This includes 138 flood policies in effect in your area along with $166,056 in total premiums.

$56,358 in premiums is the total for Lincoln, South Dakota. There are 60 active flood policies here which allows the average flood rate to be $939.

Hello Sioux Falls, South Dakota! So glad to have you stop by! You have the second highest number of active flood policies in the state: 418! The premiums written in Sioux Falls total up to $398,283 which allows the average flood rate to be $953.

Sturgis, South Dakota has 94 active flood policies with $114,943 in premiums. The average flood rate in Sturgis is $1,223.

$976 is the average flood rate for Dell Rapids and Minnehaha, South Dakota. The premiums here total to $119,030 with 122 flood policies in effect.

In Moody, Box Elder, Hill City, and Keystone, South Dakota, there are 116 active flood policies. In these areas, the average flood rate is $1,131 which includes $131,225 in premiums.

Pennington, South Dakota’s average flood rate is $1,112. The total number of flood policies is 123 and includes $136,800 in premiums. Thanks for stopping by Pennington!

176 flood policies are active in Rapid City, South Dakota. The total premiums for Rapid City are $165,506. This allows the average flood rate for Rapid City to be $940.

There are 60 active flood policies in Roberts and Spink, South Dakota. The premiums for these two areas total up to $56,800. The average flood rate for Roberts and Spink is $947.

Fort Pierre, South Dakota’s average flood rate is $920. The total premium for Fort Pierre is $97,566 which includes 106 flood policies.

Hello Stanley and North Sioux City! Thanks for stopping by to check out your flood information! The average rate for your area is $946. The written premiums here total up to $64,310 with 68 active flood policies.

Union, South Dakota, you all have the third highest number of flood policies in the state – 319! Your average flood rate is $633, which is lower than the state average. Union has $202,064 in written premiums.

Finally, let’s check out Yankton, South Dakota. Yankton has 55 active flood policies with a total of $59,519 in premiums. The average flood rate in Yankton is $1,082.